Valorant Mobile has been out for about a month now in China. It’s still too early to know if it has legs, but it’s a decent start. Per Sensor Tower iOS estimates, on a launch-aligned basis, it’s ahead of last year’s Delta Force in downloads and revenue; but it’s a far cry from the pre-pandemic launch of PUBG Mobile in China. I’ve heard vaguely that it has met Tencent internal expectations for the launch. So far so good.

I’ve yet to really play it, just like I barely dabbled in the PC version 5 years ago. (That didn’t stop me from writing a long-ish post.) I did read a bunch of player reviews, and I’ve come away with a few anecdotal opinions.

The core idea is simple, and it’s a formula that the Tencent Quantum Studios teams know well (from their successes with PUBG and League of Legends): execute an authentic (faithful), high-fidelity mobile version of a beloved PC game. Authentic (faithful) doesn’t mean blindly replicating every design decision down to the raw spreadsheet values – but it is a driving design principle in making players feel that they are playing the same game, even at the expense of something that might “fit” mobile better.

In Valorant’s case, this means that the number of rounds per match have shrunk down to “first to 8 wins” (PC was first to 13), which sacrifices a bit of the game economy flow for a shorter session length; and there are small mobile quality-of-life features such as aim-assist and visual foot-steps indicators (PUBG Mobile had the same – acknowledging that many players play without sound). But otherwise, the short time-to-kill, the general gunplay (Counterstrike-like crouch-fire mechanics) are meant to feel the same as PC, even though this type of tactical shooter is a lot more clumsy to play on mobile.

Reading the comments, it seems the game does a decent job at the above. It still feels a bit like the lower-end, fast-food version of a meal you already love, but that was arguably the same case with PUBG and LoL. “Go play the PC version if you can” is a common sentiment – that’s not a bad thing, because the mobile version is the always accessible version, for all of us who can’t play the PC version.

Unfortunately, another thing that seems to have faithfully carried over is the toxicity of the player community in a highly competitive PVP game. The “matchmaking system” remains a universal villain for Chinese players (see the frustrated Honor of Kingsplayer who sued Tencent to publicly disclose the matchmaking algorithm). Even worse, voice chat facilitates widely prevalent harassment of female players (there’s a Valorant meme where male players call female players “mom”).

I also noticed one player sentiment that does seem to be shifting. I saw a number of players complaining about the price of the cosmetics (same as PC version), and also some asking “why are we asked to buy the same thing twice?” This is an understandable sentiment, and there’s plenty of good product/business reasons (including player-focused ones) why sharing PC-mobile inventory is not the right product call.

Indeed, we went through this whole argument in the Riot team for League of Legends and the mobile Wild Rift around 2018. I wasn’t the ultimate “decider” but I was firmly against any sort of shared inventory:

While the PC game was popular in many markets globally, there were vastly more future players on mobile. If I were a mobile-only player, I would be greatly discouraged by the PC veterans and their accelerated content progression

For PC veterans, it could set false expectations that the content of PC and mobile will eventually reach parity – same champions and skins, for example. I felt the games should have the space to make unique content (and of course, collaborate on joint events where it makes sense)

Linking the two games’ inventories and thus their economies is hugely risky

The mobile version is co-developed with Tencent Quantum, which makes the economy-linking even more risky from a business rev-sharing perspective

Additional technical integration needed

And all the headaches around grey market of reselling PC accounts

Ultimately, you can abstract the argument as whether PC and mobile were 2 games or 1 game. And for Wild Rift, I firmly believed it was a different game.

Back to Valorant, I could argue that most of the above still applies as rationale to keep PC/mobile decoupled. But, it’s clear now in 2025 that this is no longer the best-in-class player experience. Natively cross-platform games, including Tencent’s own Delta Force, is educating players to demand a more seamless experience. And in turn, this is going to further reduce the attractiveness of these “western PC/console game + Chinese mobile version” co-dev deals, for both parties involved.

Several years ago I wrote about how China’s Android app stores ecosystem took a different path after Google’s exit. It’s time to briefly revisit this topic, thanks to some recent news.

The first news is related to Dungeon & Fighter Mobile’s China release. It’s been widely reported that the game generated $270M of iOS gross revenue in its first month, and Chinese media have further guessed a staggering RMB 5B ($690M) first month combined gross across iOS and Android.1 With this massive launch as the backdrop, Tencent then decided to pull the game from certain Android app stores – players will instead have to download from other stores, or directly from the game’s official website (i.e. sideloading, the behavior Epic had wanted people to adopt for Fortnite).

We can speculate the rationale behind this move. It’s probably a combination of the following factors:

The game is primarily targeting legacy Dungeon & Fighter PC players, who are tolerant to jump through hoops to play the game – in other words, there is little to be lost from reducing the distribution footprint;

The launch metrics emboldened Tencent to push for higher margins, even at the expense of new user acquisition.2

This is not the first game to get more selective with Android app stores in China. The fragmented landscape and the various tricks/schemes played have always incentivized developers to have a mercurial or even hostile attitude towards the store vendors. But combined with the next piece of news, I wouldn’t be surprised to see developer – store relationships further splinter.

The second news is about Huawei’s HarmonyOS(which started off as an Android AOSP fork), and specifically, the next major version HarmonyOS NEXT scheduled for Q4 2024, which will officially drop Android compatibility. This is a fascinating development. Most people (myself included) would say the mobile OS wars have long been over – and both iOS and Android won – so it’s intellectually exciting to see a dramatic new entrant.

Huawei has a big uphill battle, but it certainly has some advantages as well, and the current Android-compatible HarmonyOS has established a foothold already – Counterpoint Research estimates it has 17% OS share in China, slightly ahead of iOS (16%), with the remaining majority being Android. Now of course, dropping Android compatibility is still a huge gamble, but at least Huawei can present a somewhat legitimate sales pitch to developers given its market share.3 So far, Tencent has been a notable holdout, and apparently there are negotiations ongoing about porting WeChat (but I’d assume also the tentpole/cash-cow games).

Using a rule of thumb 60/40 Android/iOS split – not accurate, but not a bad ball-park guess. ↩

As an aside, I’m a bit surprised at some of the analysts’ bullishness on the title. The first month figure is certainly staggering – even by China market standards – but the title is a unique snowflake (given its years-long regulatory limbo) with lots of pent-up demand. Its performance in Korea (a big sharkfin graph) is certainly not inspiring from a longevity perspective. ↩

I’ve played Marvel Snap for about two seasons (Dec / Jan). I was late to check it out, out of laziness and lack of personal interest in turn-based card games. My quick verdict is it deserves all the praise it got, and has unexpectedly filled a “casual” competitive-PVP need that I was ready to give up.1 At the same time, the game certainly has its live-service challenges, and I’m eager to follow how the team will address them in their roadmap.

Design innovations

I look forward to the future design talks from Ben Brode and team that will shed light on their inside perspective. From the outside, I feel the game has the following significant innovations:

Core gameplay

The game’s core game reaches the vaunted heights of “easy to learn, difficult(impossible) to master” through a set of design choices that are mutually reinforcing:

Simultaneous turns, and only 6 turns total.

Simple Hearthstone-like energy system.

Small deck (12) and hand (max 7) size – by default you draw 9 cards in a full 6-turn game, which is 75% of your deck.

3-lanes board, and limited card interactivity / simple win condition: you and your opponents’ cards aren’t dueling each other, there’s no attack/block or health, and very few cards can directly destroy opponents’ cards – it’s just who has more card power in 2 out of 3 lanes.2

Each lane has a unique effect per game, from a huge and actively growing list. This RNG introduces a lot of variation which provides a unique puzzle to every game.

Card abilities fall into intuitive categories, while end-game complexity comes from cards with memorable unique effects that open up new archetypes.3

The signature “snap” mechanic, which introduces a way for players to bet and double-down on the game’s outcome, and adds a Texas Hold’em-like mind-game layer. At first I wasn’t sure whether this was a gimmicky mechanic that was negligible to the game; now I see it as a huge design bet with wide-reaching impact (both positive and negative) on the whole game – more on this later.

The sum of these designs is a core game that is intuitive to learn, has deep replayability, and requires ridiculously low time commitment for a single game (thus very easy to impulsively tap “play” again right after a game – whether you won or lost). It is addictive, with all the pros and cons associated with that word.

Meta loop

On the meta side of things, Marvel Snap also takes some calculated risks, with the results being more divisive in the community:

The game ditches the card packs / loot boxes paid acquisition model, and card acquisition is primarily from randomized rewards chests earned through engagement. The notable exception is the card bundled with every $10 season pass, and for the past 2 seasons the 2 cards (Silver Surfer and Zabu) have largely dominated the “meta”. There is also an “end-game” rotating card shop where you can spend “tokens”, an ultra-rare soft currency, to acquire a card that you’ve set your eyes on. (To visualize this: after almost 2-months F2P play I have 5000 tokens, which can afford 5 “Series 3” cards at 1k each, or 1 “Series 4” card at 3k. I can’t afford any of the ultra-rare “Series 5” cards which would cost 6k.)

While individual cards have a shards-based upgrade system,4 they do not feature stats progression or individually become more powerful in anyway – what changes is the visual presentation of the card. At the same time, I can’t label this as a purely “cosmetic” progression, since these upgrades also count towards the main progression track (“collection level”), which is where you unlock cards.

There’s a purely cosmetic card skins (“variants”) system, and the game has a large variety of styles. As a F2P player I’ve not spent any of my earned currency on skins, but I can see the appeal to the community, in terms of collecting a specific variant of a card, and then upgrading that variant deeply to create a very unique look.

Overall the progression and spend depth is very tightly controlled. You can’t buy progression outright – you can buy a limited amount of extra missions per day, so this is a “pay-to-grind-to-win” game. The developers have explicitly stated their design philosophy that players should not expect to own all the cards, and the game is about everyone owning a unique collection. I see this as a razor-sharp double-edged sword: on the one hand, with a steady inflow of new cards (one card added per week), players are guaranteed an never-ending chase and long-term motivation; on the other hand, the frustration of not having a particular card and feeling locked out of the fun can be churn-inducing.

Sampling the vocal minority on Reddit (and also watching some Snap content creators on Youtube), it feels veteran players (who’ve finished the guaranteed early game card pools of Series 1 & 2) all feel frustrated about the card acquisition pace, regardless of whether or how much they’ve monetized. This is the intended experience – only the devs will know whether the metrics support the thinking behind this choice.

Speaking about my own 2-season F2P experience, I can say Marvel Snap has one of the most generous and rewarding loops in the first few weeks of play. You get a deluge of cards,5 fast, which unlocks a lot of basic deck types and gameplay possibilities. Then things slow down considerably, and depending on how much you are grinding per day, you will eventually be soft-currency constrained (you have shards to upgrade cards, but you are out of currency to complete the upgrade). This is the main rate-limiter to the progression. At my current level (early-mid Series 3), I roughly earn enough currency to unlock one reward chest per day from the progression track, which on average means one new card every 2 days. But I often neglect the new card anyway, even if it’s a top tier one, since I likely won’t have all the cards needed to form the community-tested meta decks. This means that if I’m serious about climbing ranked, I’m playing a small sample of meta-worthy “budget” decks that I have access to in my collection state.

Despite this, I still find the ranked climb addictive – I got to Rank 60 (“Platinum”) in my first season, and 70 (“Diamond”) in the current season, after the rather brutal season reset of 30 ranks. This is still a far cry from the Rank 100 (“Infinite”) goal, which I know is do-able F2P – if only I “git gud”. Doing some napkin math – I might have played a thousand games this season, which certainly speaks to the game’s high replayability.

“Snap?”

Coming back to the “snap” mechanic specifically, as it has wide-ranging impact both on the meta and the core gameplay.

Talking about the impact on meta first – since it’s more straightforward – the “snap” mechanic adds a novel twist to the traditional MMR-based ranked PVP experience, and goes quite far to break the fatigue with the usual (and stale) “50% expected win-rate”. It does so by simply adding variance to the rewards of a single match, and giving players a great deal of control over that variance (you decide to bet, double-down, or quit). This allows for more risky or RNG-based decks to be viable in ladder-climbing. Indeed, the community quickly came up with a new metric to measure the efficacy of a deck – average cubes (ranked points) won per game – alongside the good old win-rate metric. It is quite possible for one deck to have a lower win-rate but higher average cubes than another deck.

In terms of core gameplay impact, “snap” significantly raises the skill ceiling of the game, as it is a mechanic that directly rewards game knowledge and the ability to read the game state (and predict future states). To fully exploit this mechanic, players need not only mastery of their own deck’s strengths and weaknesses, but also pattern recognition of what their opponent could be playing (based on up-to-date knowledge of the game’s “meta”,6 which basically requires consistent time commitment to the game). To paraphrase Jeff Hoogland, a content creator for the game, “snap” is the most difficult mechanic in the game, and you need to relearn “when to snap” with every new deck you play (while also factoring in what your opponent could be doing).

In addition, “snap” also greatly impacts card-play patterns, as it places greater emphasis on surprising the opponent. If the board state seems already clearly in favor of one player, and only then does that player “snap”, the other player would most likely fold (retreat) and not accept the bet. So to get the rewards for “snapping”, players must snap earlier (when both players feel they have a good chance) or when they feel they can somehow dramatically reverse the tides with an unexpected play. As a very specific example: Shang-Chi is a 4-cost card that destroys all opponent-cards that have 9 (or above) power in a lane (it’s one of the very few “tech” cards that can directly destroy opponent’s cards). It’s turn 4 (you have 4 energy to play cards with), your opponent does have a 9-power card on the board, and you don’t have better cards to play. In a game without the “snap” mechanic, it’s probably optimal to play Shang-Chi this turn so you bank the advantage and don’t waste the energy.7 But in this game, it’s could be optimal to waste the energy and save the card for a great last turn surprise.

Lastly, one downside (to some players) of the “snap” mechanic is it often takes away the big climatic finish of a game, because one player decides to retreat (and avoid possibly losing lots of cubes) rather than play out the turn. This is certainly true – the stats from this Jeff Hoogland video show that for a high-level player, 2 out of 3 games are concluded with a retreat.

Production – lean and mean

Marvel Snap clearly shows that it is made by devs with a lot of experience. As a game just beginning its live-ops lifecycle, feature scope is aggressively managed, with many “table-stakes” features still missing (for example, there is no friends-list, chat or other social features yet).

At the same time, the game already has a number of features that support live-ops longevity, while being low cost to maintain / extend:

The in-game locations (the unique RNG modifiers of each lane) is probably quite low cost to develop (it’s reusing existing card mechanics), and the twice per week “featured location” mechanic (a particular location is marked to appear more often) is a simple-yet-effective recurring event to temporarily alter players’ deck choices

The card variants / infinity splits system effectively adds unlimited personalization depth to any card, and while a F2P player like me might wholly ignore it (it feels impossibly out of reach to really care about), I would still (begrudgingly) agree that some of the end results look amazing (and desirable)

The game also already supports web-based events (i.e. an in-game banner that opens up a browser webpage in-app, showing a live-ops event). I would suspect the publisher Nuverse influenced this, as this setup (while aesthetically limiting) allows for very flexible live-ops development without the need to roll out patches (or even support from the game developer if they are not operating the game directly), and is extremely common in Chinese games

Market performance

Lastly, I wanted to take a quick look at the market performance so far. This part is probably the most speculative, since we are going by 3rd party data (estimates), and for a lot of the data you can argue both the bear and bull case.

One question is “what is the meaningful comp?” for Marvel Snap – what games are we going to compare it to? We can compare it to the top-performing games irrespective of genre, or we can just look at the CCG (collectible-card-games) genre which it clearly fits in. I don’t think there’s one right answer here; I’m quite curious how the Second Dinner team themselves think about this.

As for my personal answer, I’ll go with the latter and mainly focus on direct genre comps. A quick browse on Sensor Tower (source for most of the numbers below, and excludes China Android) shows not a lot of new games that have broken out in this space in recent years; Yu-Gi-Oh! Duel Links (global release 2017, 87M downloads to date, $758M net revenue lifetime) and Yu-Gi-Oh! Master Duel (2022, 9M downloads, $103M net revenue) are the breakouts in revenue, while Magic: The Gathering Arena (2021, 7M downloads, $58M net revenue) is helpful to illustrate the size of the audience even for one of the most fabled brands in the genre.

From this narrow genre lens, I’d say Marvel Snap‘s launch is an unqualified success: 15M downloads and $44M net revenue in about 4 months of global release. It also holds up decently (though not as well) in comparison to Hearthstone on mobile. Hearthstone saw a massive bump 1 year after global release (as the game released for tablets first, and then released to phones after a year), and would certainly have a stronger start than Marvel Snap. In any case, Marvel Snap is showing it can absolutely go up against the biggest names in its genre.

But how about from the broader lens of all games, ignoring genre? I’d argue the team should also be proud of themselves. On Sensor Tower, I looked at the top mobile games by revenue for the past 24 months, filtered for games that were released within the last 3 years (i.e. filter out the evergreen games like Honor of Kings or Candy Crush). On this list, the top 3 were Lineage W with a massive $734M net revenue (from only $4M downloads – and majority of that revenue was from South Korea alone); Royal Match with $631M net revenue from 83M downloads; and Cookie Run: Kingdom with $260M from 22M downloads. Yu-Gi-Oh! Master Duel was #13, while Magic: The Gathering Arena occupied #22. Marvel Snap is currently at #29, and will certainly go up in the rankings. This is an impressive feat for the first game of a new studio, regardless of the pedigree of the talent.8

As a minor point, the concurrency chart for Marvel Snap on Steam shows a steady game with very sticky retention. It’s hard to read too much into this, as this is a tiny fraction of the total player base, but one reasonable hypothesis could be that this is a decent sample of the game’s most hardcore players (who will actually multi-home and play this mobile-first game on PC), and the steady trend line is encouraging.

For the bear case, there is certainly room for concern in the rapidly declining downloads: at ~250k weekly downloads, it’s comparable to Hearthstone‘s weekly downloads 15 months after their phone release. But I’d say there are too many unknowns here to really know what’s going on (what’s intentional / expected, what’s reversible). The game isn’t live in China yet (and probably won’t be, for a couple of years), so the Hearthstone comp isn’t apples to apples. The publisher, Nuverse (part of Bytedance), should have lots of money to fuel UA, but they are an unproven organization (per Sensor Tower, this is already the biggest game they’ve launched, in terms of downloads). And I don’t know what is the actual division of labor between Nuverse and Second Dinner. In any case, revisiting the data in 6 months will give a lot more clarity on the game’s long-term legs.

Mostly due to life circumstances – we came up with the term “gamer soul, adult responsibilities” years ago at Riot to describe this. ↩

The math can still get quite complicated with more advanced cards and combos. ↩

There is a concern about the long-term design maintenance of cards, since these unique cards often introduce exponential levels of effort to balance and constraints to future card-design space – for example, the January season pass card Zabu, which reduces the cost of all 4-cost cards by 2; or Mister Negative, which when played inverts the cost / power of each card in your deck. ↩

As of this writing – you unlock 97 out of the game’s total 200 cards once you are Series-2 complete ↩

What decks / strategies are popular in the community; not to be confused with the design-lingo “meta loop” that usually refers to the game’s long-term systems. ↩

I’m on a late summer vacation and wanted to get back to writing. Sheep a Sheep provides an easy topic, even though it’s not usually the type of game I would comment on.

The short story: Sheep a Sheep is a hyper-casual match-3 puzzle game, available as a mini-program (roughly HTML5-based) within WeChat. The game has become a controversial viral sensation in China the past week. (Here’s a write-up about the game for more context.)

The controversy stems from a few areas. First, there is the question of whether this game is a copy of other works. The base gameplay is similar to mahjong solitaire. Many people have also pointed to the game 3 Tiles as the source of inspiration – indeed, 3 Tiles itself has shot up to the top of the App Store download charts in China on this unexpected tailwind (so, should they be thankful for getting ripped off?).

Second, the core hook of Sheep a Sheep is ethically shaky, to put it mildly. The game is labeled as an “ultra-hard puzzle game where only 0.1% of gamers can win.” After a quick tutorial level-1 where players are taught the match-3 mechanic, players are immediately presented with a procedurally generated level-2 that in vast majority of cases are mathematically impossible to complete. By watching ads – this is the game’s sole monetization -or sharing links to the game via WeChat, players can access a very limited number of power-ups that can improve their odds slightly – but usually this is not enough to actually win.

The game employs a proven bag-of-tricks to entice players to try for the impossible win. Even winning once is huge bragging rights, which plays right into the game’s viral referrals – “have you won once yet?” Furthermore, there’s a province-based leaderboard right on the game’s home screen, and by winning you contribute to your province’s rankings on this leaderboard. And winning games also gives you currency to buy cosmetic items, which of course are more avenues to show off and brag. All of these are battle-tested mechanics in China’s top games, and immediately familiar to players.

I’ve played maybe 10-20 rounds, and in a couple of tries I felt I was close to a win – but it’s hard to know for sure since the tiles can stack infinitely and thus you never know for sure how many tiles are left. Despite knowing that this game is in many ways a scam / hoax and the odds are hopelessly stacked against me, I felt compelled to play more, to just win once; and I gladly clicked to watch the ads which raised my chances by an infinitesimal amount (99% of the ads shown to me were for Pinduoduo). I guess this is similar psychology to people buying lottery tickets or playing slot machines.

In contrast – 3 Tiles is certainly a better-made game, with superior aesthetics and a traditional free-to-play puzzle-game difficulty curve. Like many other puzzle games, it has hundreds of levels and I cruised through the first dozen levels. My only complaint is the game’s high frequency of ads – an ad is played before every level and there are some UI “dark patterns” during the ads to trick click-throughs.

And this is where this “case” gets interesting for me. Comparing the 2 games, it seems like a no-brainer that players should choose the better-looking game where they can actually finish the puzzles, instead of the deceptive and poorly-made game where 99.9% of the time you are set up to fail. If you were to bet on the outcomes of the 2 games ex ante – say, you are a publisher or an investor looking at these 2 game pitches – it would seem crazy to bet on the latter. And yet, in this case we know the latter is the winning bet by far. What, if anything, should we take away from this case?

Well, “maybe there’s not much to really take away” is a reasonable answer in my opinion. No one expects Sheep a Sheep to have longevity – after realizing the game’s objectively bad (intentionally deceptive?) puzzle design, many people feel tricked and there’s likely a backlash.

At the same time, from a “jobs to be done” perspective, we should realize that 3 Tiles and Sheep a Sheep target entirely different needs (and thus different audiences): 3 Tiles serves the motivations of the traditional puzzle-game demographics, while Sheep a Sheep is about serving a flavor-of-the-month novelty to the Internet at large. The necessary ingredients of such a flavor-of-the-month novelty could be: illusion of skill, high element of randomness/luck, and a subversive x-factor that drives virality (“only 0.1% can do this – can you?”); it is coincidental that the 3 Tiles gameplay could be successfully twisted into this recipe.

For “serious” game devs, perhaps there’s some room to interpret Sheep a Sheep as yet another case for subversive design choices. Making the 2nd level of your game incredibly hard is a subversive decision, and maybe it does make sense in some very rare set of conditions.

[Sep 27 update]

I thought it was worth a minor addendum, one week after the original post above. A couple of things happened:

First, it seems the devs drastically reduced the difficulty of the game – by drastic, I mean that the odds of winning went from 0.1% to 5% (illustrative numbers, but you get my point). The net result is that in absolute numbers there seems to be a lot more players getting a win every day (in the above screenshot, there were already 500k winners during the day), but percentage-wise it still feels like a fool’s errand.

Second, I finally got my personal first win, after maybe 100 tries? Anyway I’ve played for ~10 days and this is the first win. With my win I got a cosmetic (the constructor sheep above). With this win, I also finally realized that the game also emulates Wordle‘s “a puzzle a day” format – once you’ve won a round, you have to wait 24 hours before you can challenge again, in effect setting up an appointment mechanic.

Xbox announced a Game Pass deal with Riot Games (my previous employer, I left in 2019). The deal covers all of the live service games in Riot’s portfolio, across PC and mobile platforms.

I have a few thoughts in reaction to this news. The first is the surprisingly large value Riot is putting on the table. This is not a small experiment; Riot didn’t go the safe route of starting with one game and deciding to expand or not based on the metrics. And even if it were just one game, say League of Legends, the monetary value of “All champions unlocked” is not trivial. As a quick “valuation” exercise:

Buying them all outright (even though few players do this – you can earn soft currency and unlock champions by playing) is easily hundreds of dollars – you can google for various answers, players have done this math before.

An alternative comp is to look at Asia, where “all champions unlocked” is a B2B product that PC cafes in Korea and China pay Riot for. If you assume Riot charges a Korean PC cafe $0.2 for every hour of this service, and on average players play 30 hours per month (both of these are like 10-year-old stats in my head), then “all champions unlocked” is by itself a $6/month service.

However you look at it, it seems that Riot is offering a ton of value here – so much so that, if you are a dedicated fan of Riot’s games, you should sign up immediately for Xbox Game Pass just for the Riot benefits alone.

This sparks an interesting offshoot question – instead of working with Microsoft, why didn’t Riot roll out its own “Riot Games Pass” instead? I would imagine this scenario had to have been part of the internal strategizing. And that would feel more in line with the M.O. of the Riot Games I know circa 2015 – doing it alone, desiring total control of the player experience.

I don’t have any inside knowledge, so I can only venture some guesses based on looking at the exchange of value in this deal:

From a player acquisition perspective, it seems more likely that Riot is funneling players to Microsoft – League announced 180M MAU last year, although a significant portion are players from China, which Xbox Game Pass doesn’t officially serve; while Xbox Game Pass last announced 25M subscribers. But Riot does also gain a new channel where new players could flow in, and it may be a previously underserved (more console-oriented) player-base. Thus Riot stands to benefit from all future Xbox Game Pass marketing, as a % of future Game Pass subs could convert to Riot players.

Based on the above, I would imagine there’s a sizable monetary component to the deal, flowing from Microsoft to Riot. I’m not a BD person, I don’t have a good sense where to start to try to model this component. It could be a fixed per-year amount. It could be calculated based on actual player engagement (some sort of revenue share / pre-defined payout based on metrics). It could be a combination of the two.

To Microsoft, I also think there’s a Game Pass content strategy component to this deal as well – having popular live-service games, like Riot’s portfolio, acts as a natural buffer against AAA seasonality, and probably helps with smoothing out churn.

Another interesting part of this deal is the mobile games included. This has the effect of providing an off-platform (iOS / Google Play) way to monetize a mobile game’s content, though in the past this was usually done by the game’s publisher directly, as opposed to another platform like Microsoft here. It will be curious to see if there’s any response from Apple & Google, especially if Microsoft starts rolling up additional mobile games into Game Pass and could threaten to end-run IAP regulations.

From Riot’s perspective, I can also think of a number of risks to this deal that needs to be managed:

The monetary math: does the inflow from Microsoft cover the possible loss of all future champion revenue (to use League of Legends as an example)?

The game economy and player behavior implications: during my time at Riot, I felt the long-held internal view was that providing all champions for free (which is what DotA 2 does) has negative effects on players’ onboarding flow, matchmaking quality, sense of ownership and progression. This deal seem to override these concerns.

In summary: this deal took me by surprise, but I think it could make sense for both parties. It would be fascinating to follow how this impacts both companies going forward.

Genshin Impact has had a great global launch – indeed, I struggled to come up with some good comps on Sensor Tower as it has really stormed out of the gates. In terms of launch revenue, I actually couldn’t recall a better game than Pokemon Go. See below launch-aligned revenue graph:

If we just look at China, where it’s easier to compare apples-apples (at least for iOS only, since Sensor Tower doesn’t track China Android), we have an early 3-way tie across AFK Arena, Brawl Stars and Genshin Impact – as some of the best launches of 2020:

As a side note – AFK Arena’s $60M launch month on iOS in China (in January before Chinese New Year), is the best new mobile game domestic launch this year as far as I can tell. (The usual caveats about lack of China Android estimates apply…)

But, Genshin is not just a mobile game – in China, it launched on PC first on Sep 15, a full two weeks of early access. I still find this an unusual choice – the most affluent, hardcore gamers rushed in on day 11, but the negative reviews came in almost instantly. Snobby PC/console gamers mocked the game’s lack of polish and lower graphics fidelity compared to premium AAA titles; whereas mobile gamers looking for a progression head-start via PC immediately raged at the poor gacha loot table. They didn’t hold back their emotions on Taptap:

The poor reviews didn’t seem to impact sales much (and the Taptap crowd is hard to please). It’s also interesting to contrast this reception with the western audience reception – there seems to be a lot of voices expressing surprise that the game offers so much content and is free.

In any case – it’s very early days yet as we are barely two weeks into the official launch, but all things considered it’s a great start for Genshin Impact. It will be fascinating to see how the game trends over the next few months.

Core gameplay

The game is quite well-reviewed on Metacritic (though a small sample size), and deservedly so. The scope of the open world, the combat system, and the character roster (and their visual presentation) are impressive.

The game is most fun (I’m currently Adventure Rank 27) when you are doing the dependable open-world loop: you start out with a particular objective (maybe a quest, or just a point-of-interest you spotted in the horizon), and along the way you get side-tracked by numerous side content. There is a lot of side content: collectibles, side quests / daily missions, environmental puzzles, loot chests that respawn periodically… You get the picture.

Genshin Impact certainly takes a lot of inspiration from Zelda: Breath of the Wild‘s open-world formula, but ventures far enough to end up in its own place. The biggest departure is combat: Genshin referenced the elemental interactions from BOTW, and converted it into a catchy combo system that still feels intuitive enough. It can get repetitive, but it’s still satisfying to set up an explosive fire-lightning combo (for example), and there are hints in the equipment system (I haven’t gotten far enough yet) of intriguing build possibilities.

Personally, I’m not too concerned with the graphics fidelity on PC – I’ll always take smooth frame-rate over graphics quality, and this is where Genshin does not fully deliver. On mobile, I can’t run reliably run 60fps on an iPhone XS Max (even when I toggle everything down); and the game’s min-spec on iOS is iPhone 8 Plus, which suggests dev challenges with performance optimization (in comparison – PUBG Mobile‘s min-spec is iPhone 6s).

I do want to talk a bit about gameplay feel and polish, where Genshin is behind its PC/console peers in some areas. As a player, I found myself often wrestling with the game’s character, camera and controls (the “3Cs”), on mobile (more egregious) as well as on PC. Some examples of jank:

Ranged aiming feels finicky in general, even on PC with mouse; sensitivity settings are too coarse in my opinion. And for mobile / PS4 there should have been some aim-assist support (even if they can be turned off).

The camera has janky movement at times – as a tiny example, when you fall and roll forward, the camera takes too long to recover from facing downwards, and requires a manual adjustment2.

Some characters have attacks that dash through the enemy, which would require you to rotate the camera 180 degrees to see the enemy again. This is in my opinion dangerous design space for a 3rd-person mobile game with virtual joysticks.

Similarly, the Traveler’s ability that creates a giant rock is also dangerous design space in combat: this is a climbable rock that can cause unintended player interactions; and it often displaces enemies to the top of the rock, where they don’t seem to know how to get down (and thus severely disrupting combat pacing). The fact that the ability is aim-able is also stress-inducing on mobile.

Enemies who are displaced from the combat area (for example, falling off a cliff) get reset (with full health), which is often frustrating.

I’ve also found the game’s boss fights tend to have more jank and annoyances. For example, the first major boss fight below:

There’s a bunch of things here that irritated me (and yes, my skills are probably below-average…):

The level requirement stated upfront was a bit of a misdirection, as you are given a trial character with their own level, and the whole fight is primarily designed for that character.

Unskippable cut-scenes, which is a pretty big no-no if players have a chance of having to replay this fight several times (which I did…).

The flight combat sequence starting around 1:30 has readability issues, with the backdrop that is quite static and the boss always center-screen – the first 2 times I played this fight, I didn’t understand I could actually fly towards the pick-ups (I tried maneuvering and felt I couldn’t change direction).

The final phase has a custom camera angle (side-scrolling), which is a bit jarring as most of the game you are not driving your character’s movement primarily with left/right input. Combined with the ledges, this created a level where I fell off quite a few times – while not lethal, it was very annoying for combat pacing.

Over time, the player learns to work around these problems, but there’s clearly a gap in terms of the developer’s capabilities, sensibilities, and/or priorities – these are the 20% issues that can take 80% of the time to solve to get that AAA polish.

Progression and monetization

When it comes to progression and monetization, Genshin at a high level shares a lot of the generic Chinese mobile RPG template (of which AFK Arena, mentioned earlier, is the current best-in-class example).

The basic formula of such games is a deep progression system (with layer upon layer of different stats to chase), with stringent upgrade gates interlaced with periods of relatively smooth leveling. The stringent upgrade gates provide heavy incentive to do the daily/weekly grind for resources (certain key resources can only be farmed on specific days of week). And the sheer amount of dimensions to progress (amount of characters + depth of each character) converts into aggressive monetization design, where ultimately cash can be turned into characters (through gacha), upgrade resources (directly purchased), stamina for grinding resources and so on.

This is the rinse-and-repeat formula that hundreds of Chinese games have used – Soul Hunters, Naruto, Honkai Impact 3rd, Onmyoji, Arknights, AFK Arena, to name just a few of the biggest over the past decade.

The marriage of such a formula to the open-world gameplay in Genshin is at first jarring – the early leveling experience of a player who immediately spends several hundred dollars on gacha is going to be very different (and arguably for the worse – as all sense of early pacing is out the window) from a non-spender. I know such a gamer – he is trained to plunking down a few “648”s (by convention the most expensive SKU in the cash shop, roughly $100) any time he starts a Chinese mobile game – and were it not for social peer pressure, he would have churned several times by now (despite spending almost $1k already…).

After 20 hours in, when I’ve largely picked up the various complex systems and are somewhat invested in some characters, the disconnect starts to go away. It becomes very clear that access to a lot of fun gameplay is gated behind monetization – the 5-star characters that everyone is enamored with are not going to come easily (and even if you unlocked them – you need so many duplicate copies to fully level up their powers). You can still have a good time – but you will be missing out on a lot of gameplay possibilities.

Regardless of whether you monetize or not (or how much), the grind is still somewhat egalitarian3. That’s the other funny part of this RPG formula – it demands both money and time.

Usability pains

One part I’d like to complain loudly about is the game’s UI/UX and usability issues – not only because I suffered lots of irritations here, but also I feel there’s a hard-to-measure (but perhaps material) impact on the game’s engagement. Genshin is already overloaded with design complexity (as is typical with Chinese RPGs), and the usability issues amplify the cognitive load.

I already discussed some issues in the gameplay section above, but here are a couple of examples specifically about the UI. This part of the discussion is quite tactical.

First, I found it baffling that the map and quests UI were not integrated. They are activated via separate buttons on HUD, and don’t link to each other.

On the world map, you actually can’t see available quests (with the exception of the 4 daily quests). You have to “track” a quest in the Quests UI for it show up in the map. This would be much less of a problem if the Quests UI were available as a pop-up / side-bar in the Map UI. But currently, you have to jump back and forth across 3 UI screens to complete a simple action of “select a quest and find nearest teleport point”.

The Map UI is also lacking functionality in some other basic areas. For instance, you can place custom nodes on the map to keep track of points-of-interest (players use it to tally the important collectibles, for example). But you can’t “navigate” to a custom node, which feels like a pretty useful interaction.

For an open-world game, the Map feature should be something that really emphasizes ease of use – help you make decisions about what to do next, and get out of the way as fast as possible, so you stay immersed in the world. But in Genshin it currently is subpar compared to most contemporary open-world games (e.g. Ghost of Tsushima for a very recent example). I honestly can’t remember the last time I was so confused at the map feature of a game in this genre.

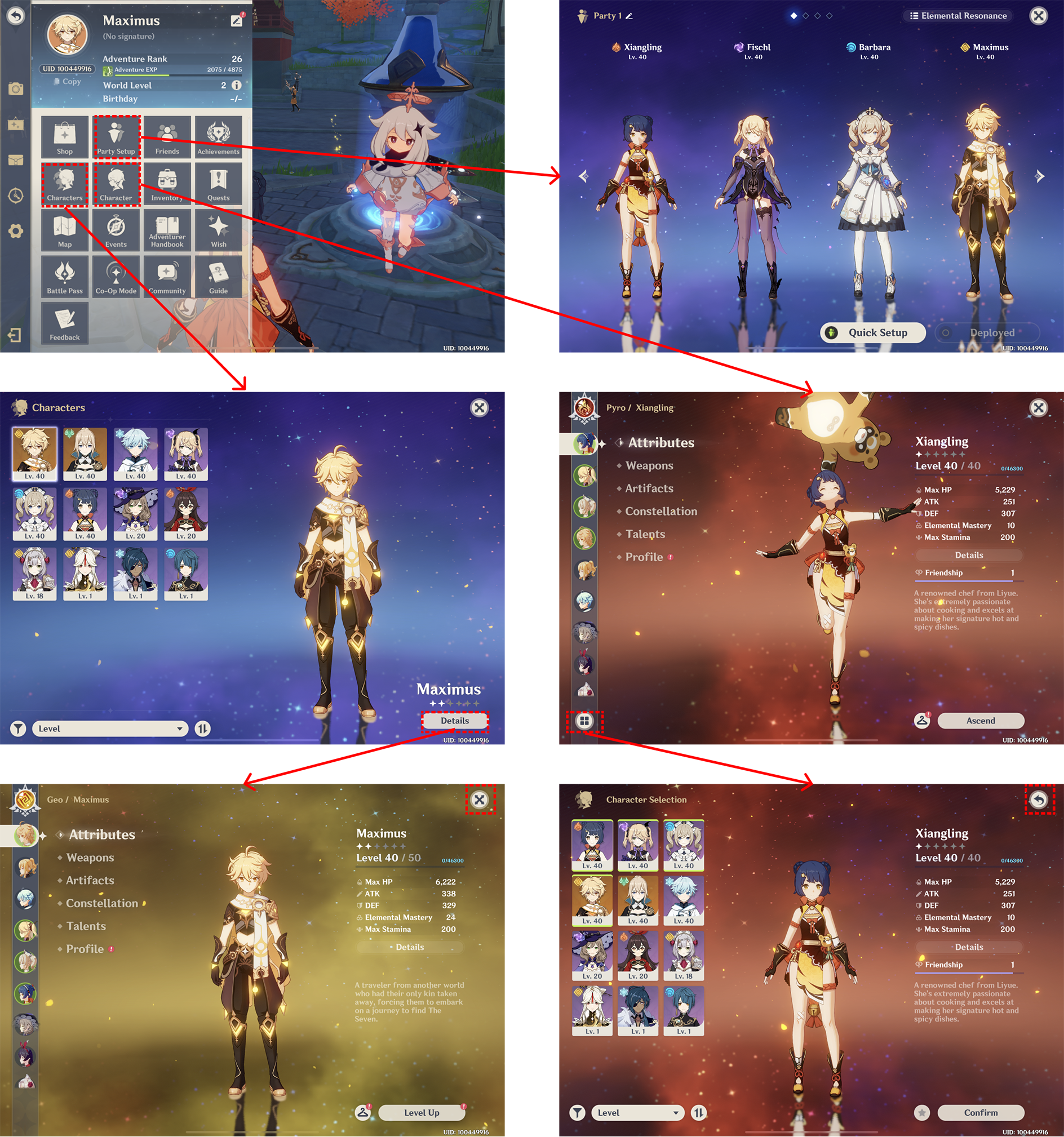

The second UI issue I’d like to talk about is the various screens related to character and team management – I did a quick navigation flow to help illustrate my point:

Broadly speaking there are 2 distinct needs: roster selection and character management (leveling, gear management, skills upgrades etc.). So having separate menu entry points for “Team setup” vs “Character” does make sense, even though they could be combined in an alternative flow. But I find the “Characters” vs. “Character” flows puzzling – they are largely made up of same/similar screens (just with reversed navigation), but there are some weird UI inconsistencies:

The ordering of characters is inexplicably different – in “Characters”, sorted by level by default; while in “Character”, the active roster is shown first, then the rest by levels.

The “Characters” screen and the “Character selection” pop-up also make for an interesting comparison: these two screens have largely the same layout and high level purpose (view list of characters, select one to navigate to), but have numerous small UI differences (list of 4 in a row vs 3 in a row; blank space vs. right bar of character details; “X” vs “back” navigation buttons…).

I might sound nitpicky here, but these small inconsistencies add up to unnecessary cognitive load (forcing the player to actively think), which begs the question of why do these 2 largely redundant flows exist?

To me, this is a reflection of lack of holistic game polish, and perhaps related to the production culture, which I’ll do some extrapolation and speculation below.

Closing thoughts

I wrote a post last year “Assessing China’s game development capabilities.” I think Genshin Impact is a continuation of the trends I discussed there, but it should also be proudly celebrated by Chinese developers as a product breakthrough in original IP on the global stage.

It succeeds in part due to its sheer audacity in vision and content scope – original IP, open-world, cross-platform (with mobile as the core), and years of live-ops content runway. miHoYo is well positioned to tackle this, having honed its IP creation skills in the Honkai franchise, and with good access to China’s “industrial scale” mobile production capabilities.

I do think it’s a “quantity over quality” approach, as I feel the game clearly prioritized volume of content (and future expansibility) over polishing details. But again, this is the proven formula for Chinese devs – getting the fundamentals barely good enough, then production scaling like crazy. Whereas western devs tend to be wary of the content treadmill (e.g. WoW’s expansion cycles), Chinese devs seem unfazed about embracing it. They don’t enjoy it – but they are more willing to grind it, and for the successful games, the economics seem to pay out well. While we don’t know for sure currently, I expect Genshin to have a stream of major updates planned already (the next one is probably close to completion by now), and the update cadence may again surprise the global audience4.

(UPDATE: the update schedule was actually announced, and it looks like initial reactions from the hardcore community globally was disappointed. See this reddit thread.)

Where Chinese devs should/need to grow further, in my opinion, is the discipline, thoughtfulness, (and frankly) prioritization of better UX5. This is not easy to do – in my personal experience, I’ve found Chinese devs’ strong production-scaling tendencies and general haste to be big barriers for holistic game polish. But as the market, and gamers, get more demanding, I expect higher emphasis here in future, which may force shifts in development models.

Before I forget, a couple of things to highlight that are part of the game’s breakthrough:

First is localization: I played the English version for a while before switching back to Chinese, and I thought the English localization had very high production quality, made by a veteran team of writers and VO cast.

Second is the music: I love it. It’s clear no expense was spared in music production, and the soundtrack is lovely. However, sometimes the music transition triggers seem a bit ungraceful (again, perhaps one of these polish cases).

At a macro level, I think it’s safe to speculate that Chinese devs are going to have even bigger ambitions post-Genshin, despite significant external headwinds (China-domestic regulations, state of economy, global geopolitics). The NA/EU market is the last frontier geographically. It will also be interesting to contrast East/West approaches to cross-platform: Chinese devs will be grounded in mobile-first (otherwise they leave a lot of money on the table with the China-domestic market), whereas western devs will tend to prioritize PC/console à la Fortnite.

As a sign of Chinese gamers’ constant vying for status (which is a huge part of their motivation for gaming), gamers actually complained loudly that miHoYo opened the servers a couple of hours ahead of schedule – they felt betrayed about missing out on snatching a sexy low-digit UID. ↩

I don’t remember specifically, but this was probably one of the ear flicks that caused me to give up on using a controller on PC. ↩

If you spend for stamina, you earn the privilege to grind more. ↩

While simultaneously being criticized by Chinese players for being too little too slow – such is the diminishing returns. ↩

An unfashionably late (as usual) post about 2019 and the big games industry themes that I found interesting. Similar to last year’s post this will be focused on the China perspective.

Further global footprints

A continuation of the past several years – 2019 saw Chinese devs & publishers continue to expand globally. Representative titles such as PUBG Mobile continued to gain ground, ending the year as one of the year’s biggest games in terms of revenue and active players. (Note that the game’s revenue is going to be meaningfully higher than popular estimates, as the game is integrated with various non-Apple/Google 3rd party payment channels that are significant – or even the majority in terms of payments market share – in Southeast Asia and other emerging markets.)

Similarly, Garena’s Free Fire was also raking it in – primarily from Southeast Asia and South America – reporting over $1B in lifetime revenue since its 2017 launch. (Garena is based in Singapore, though Free Fire‘s dev team is based in Shanghai if I’m not mistaken.)

To sum it up – real-time competitive PVP mobile games (by Chinese developers) PUBG Mobile, Free Fire and Mobile Legends are now household names across the Middle East, South and Southeast Asia, and South America.

It wasn’t just about emerging markets – Call of Duty Mobile blew open the gates to the prestigious North American market. While it has a lot to work to do to lift monetization, it is likely changing the perspectives of the gamers who have the most platform choice (and who have been the most snobbish towards mobile gaming).

IP partnerships

Staying with Call of Duty a bit more: I’m very confident we are going to see a lot more of these types of East-West IP partnerships, purely out of necessity. Simply put, I’m not aware of any western studio that have the proven capabilities today to execute in-house against the development and publishing of a mobile game similar in technical complexity to PUBG Mobile or Call of DutyMobile. Epic and Fortnite is the closest example I could think of – but even there, their mobile optimization and global footprint pales compared to the above.

In a way, these partnerships, or talks of such partnerships, are nothing new – for example, over the past few years, Blizzard have certainly talked several times with Netease, Tencent et al about mobile projects around all of their various IPs. (Personally I’d love to see a Starcraft game on mobile.)

But what is likely new is the seriousness of these conversations now – the Chinese devs have a lot more proven successes to point to, and the western IP holders are a lot more educated about the proven market demand. So expect to see a lot more of these, and possibly a lot sooner than you’d guess.

Chinese design innovations

What I personally found most interesting last year though, was the startling success of Chinese devs when it came to their biggest deficit traditionally – game design innovation. It was truly a break-out year.

Each of these games were hugely successful in 2019 in some way. Auto-Chess spawned a esports genre after itself (and certainly disrupted the landscape of adjacent CCGs). Archero caught lightning-in-a-bottle with its surprisingly elegant (and highly addictive) core combat. Arknights and Punishing: Gray Raven both represent best-in-class games in their respective genres today (tower defense and 3rd-person action), on top of stylishly creative original anime-IP (interestingly, both were apocalyptic sci-fi in theme). And mobile developers couldn’t seem to stop talking about AFK Arena, a brilliant iteration from Lilith Games on a genre they themselves largely created half a decade ago.

Also – almost all of these games on the list come from relatively unknown developers (the exception being Lilith). This certainly feels like the silver lining in the deep winter that Chinese devs have inhabited the past 2 years (venture funding has been nonexistent since 2017, and the game license issue has froze up the domestic market). I look forward to the many pleasant surprises that the surviving studios will bring to market – whether it’s aspiring blockbusters from known studios such as Genshin Impact (by miHoYo), or the next wave of indie hits.

This seems to be a re-occurring discussion I have on this blog, but with the release (and early positive reception) of Call of Duty Mobile (developed by Tencent Timi – J3 studio; published worldwide by Activision and Garena in respective markets), it’s worth refreshing this conversation.

Similar to PUBG Mobile, Call of Duty Mobile seemed to immediately receive praise for its technical performance. Players are wow’ed that “this is playable on mobile”, “it runs so smooth!” Etc. It is indeed an impressive feat, with no doubt lots of hard labor and ingenious solutions to hard problems. In its sum it’s Chinese developers reaping the rewards of their half-decade investment in mobile development at AAA scale.

Framework sketch

If we take a step back and snapshot Chinese developers’ capabilities in the global games industry value chain, we might get something like this (excuse my crude hand-drawn graphic):

China’s capabilities in the global games industry value chain

Here, the value chain component labels are intentionally generic (I’ll come back to this later). And the artificial separation of “Design” and “Manufacturing” are divergent from reality, but you get the rough idea.

The main observations I tried to capture are:

In the console platform, China has traditionally only had a minimal / partial “manufacturing” role, in insourcing or outsourcing (e.g. western developers’ China studios that help their western teams finish their games; or large outsourcers like Virtuos). A lot of this is due to the lack of a home-grown market

In PC, Chinese developers made lots of games, but they were generally non-AAA and in the lower end of the market (for example browser games). There were various attempts at shipping these games to a global audience, but nothing that became a cultural phenomenon

In mobile, Chinese developers are leading the charge on almost all fronts (with exception of “design” which I will break down in a bit), pushing the technical boundaries as well as going deeply to emerging markets that have historically been neglected by most publishers. Their capabilities in manufacturing and distribution are industry-leading

Now coming back to why I generically labeled it “manufacturing” and such: this is thanks to a quick chat I had with a co-worker this week. My colleague has an education background in industrial management. When I started discussing with him what I thought were the strengths / weaknesses of Chinese developers, he instinctively mapped it to industrial manufacturing – “it sounds like they are very good at running the factory – operating manufacturing processes, solving the production line issues, ensuring output quality etc. But these production line engineers tend to be terrible at new product development because they are focused on totally different sets of things.”

I thought this was a great insight. And yes, game developers tend to know whether they enjoy and are good at making new games or working on live titles (very few developers are great and passionate about working on all stages of a product’s lifecycle). But mapping it back to an almost archaic manufacturing-line metaphor really helps distill the point.

(One other benefit about the generalized industrial labeling is we are reminded to explicitly reference what has happened in other industries – for example appliances and consumer electronics.)

A side-bar about Design

So, to the part about “design” and China’s capabilities here. First off, here I’m using “design” in the more general sense (and it’s probably a poor word choice on my part) – it refers to loosely everything to do with new product development. I think this is by far Chinese developers’ weakest area. Thinking out loud here, there’s a few factors why:

China has a relatively shorter history of game development, and the industry has always been skewed in narrow areas (online f2p)

Much of China’s recent growth has been in perfecting the production line – working around harsh memory constraints to realize a feature, designing a networking model that supports twitchy real-time multiplayer gameplay in unreliable mobile network conditions, making the game run on 5-year old phones, efficiently integrating with a long list of social networks / app stores… When most teams have focused on being the best production line team, they lose the mindset for new product development

China’s shorter-term planning and rampant clone culture results in less value placed on original design, and thus less exercised muscles

And to some extent, China’s education system and societal values are detrimental to fostering type of talent that excels at creativity and independent thinking (this is obviously a huge topic in itself, and it’s easy to overstate this factor’s impact; but I think it does exist and should be listed)

Known unknowns vs unknown unknowns

So, coming back to Call of Duty Mobile. In many aspects it’s a great product and the team should be proud of what they’ve accomplished. It’s a great showcase for the Manufacturing prowess of Chinese developers.

From the extremely few anecdotes I’ve heard about this project (casual conversations with folks from both Activision and Tencent), the Activision team was fairly hands-off with the game’s development. (In Activision’s IR comms, the game is also described as “Published by Activision, and developed by Tencent Games’ award-winning TiMi Studios”.)

I think in this specific case, this IP-licensing model works, because there was likely little doubt what the desired gameplay experience is (bookended by PUBG Mobile on mobile, and the decade-plus refined Call of Duty experience on console).1 That is to say, the challenges in this project are mostly known unknowns – “how do we solve the input challenges?”; “how do we recreate these iconic CoD maps to fit the memory budget?”; “how do we ingest Activision’s raw assets into our assets pipeline?” etc. Or really, mostly known knowns, as Timi has already overcome most of these challenges in their previous (now canceled) PUBG game.

For this type of known unknown work, as it relates to mobile games, I doubt you can find more capable developers than Tencent and Netease. And I expect them to find further success with other IP licenses, for example, the rumored Apex Legends mobile game, or even the negatively primed Diablo Immortal (which I still cautiously hope will defy expectations). And I could imagine them tackle something like Destiny or World of Warcraft2.

Basically, anything where there’s a beloved IP on top of proven gameplay (that can be adapted to f2p)- call Tencent / Netease and get it on mobile. Forget your own biases about what should / shouldn’t be on mobile. The Chinese teams will solve all the seemingly impossible challenges, and the game will reach an otherwise unreachable audience (the billion plus players in emerging markets, the older / younger gamers for whom mobile is a much better lifestyle fit than console / PC).

But for exploring unknown unknowns, or in our industry, creating games that doesn’t have a clear reference or have so many new ideas ingested that it has become something evolutionary, I still think the heavy-weight teams in China generally lack the DNA, culture and org structure to effectively pursue. Games like Zelda: Breath of the Wild, Portal and Clash Royale, to name a few random examples.

Thus as a closing thought, the marriage of global Design capabilities to Chinese Manufacturing seems like a literal $10B opportunity (if not more). It is clearly incredibly hard to do, starting from a lack of talent – people who are passionate / knowledgeable about game dev, speak the languages, and are adroit at bridging the cultures. But I’m quite optimistic that this will improve over time. Perhaps Apple’s “Designed in California. Assembled in China.” Is one gold standard we could look at.

Before PUBG Mobile there were perhaps lots of questions of “why would players want to play that on mobile?” But now that’s been answered loud and clear by literally hundreds of millions of players. ↩

My first camera was a gift from my dad, when I was about 10 years old. I vaguely remember it was a Pentax point-and-shoot, and it cost around £200 (?), which would be $300 in the mid 90s and over $500 today. I was not an avid photographer, but I did burn through some rolls of films when my parents took me to events such as the Edinburgh festival.

Fast forward some twenty-odd years, and my 3.5 year-old son, who’s unsurprisingly obsessed with Disneyland, has learnt to ask for our smartphones when we go on his favorite ride “It’s a Small World”. He would eagerly snap photos of every part of the ride. I thought it was really cute, and I’d certainly want to encourage his creativity, except I wouldn’t want him to accidentally drop a $1,000 phone in the water.

It so happened that same day a friend posted a wechat moment gleefully sharing her son’s new kiddie camera. Talk about viral marketing. So I started searching Amazon for camera toys. After hearing from my friend the detailed specs of the camera she got, I narrowed down my search and made a purchase. It arrived last week and my son’s been busy.

Front and back dual camera, 12 megapixels; 1080p video; flash

32G micro-SD card included

15 fun cartoony frames (borders) to create funny photos/selfies directly

Wifi and smartphone app for browsing photos wirelessly

Overall very kid-proof design

(Running on modified Android)

Meh picture quality…

The pictures are quite meh (probably a mix of the lens and the lack of sophisticated post-processing), but that’s almost besides the point for a toy for pre-schoolers. Toys are often about make-believe: a fake facsimile for the real “thing”, whether it’s cars, dolls, a kitchen set or a hardware bench. But we now live in a world where it doesn’t have to be just pretend – it’s now cheap enough to just give kids the real thing, in a package designed for them.

In a way this is incredibly liberalizing: kids are more than ever equal to adults, and can access and utilize similar tools for creativity and expression. Expect to see more young photographers and film-makers. (Side-note: this reminds me of the original Super-8 cameras, that many renowned film-makers such as Steven Spielberg speak fondly of.)

One other observation: this toy is a simple repackaging of existing mobile hardware / software, with a customized form-factor. And that’s why the components are cheap. What other gadgets that target niche user-cases are possible?

This simple mobile game has been quietly popular in my part of the Riot office recently, and I found myself quickly spending 2 hours a day on it, so I thought it deserved a quick write-up.

Reading the credits and the publisher’s website, Archero is developed by a small indie team (11 people listed in the credits, including 2 programmers, 4 artists and 1 game designer) in China. The publisher HABBY has a stated strategy to identify high quality indie productions from China and bring them globally. (I’m generally a fan of this approach and think there’s an arbitrage opportunity here currently.)

Core gameplay

The core gameplay is deceptively simple but with a sharp design insight. This is an action roguelike dungeon crawler, where you control a character that can perform ranged attacks. You only control the character’s movement; when the character stops moving, he attacks based on AI auto-aiming. The insight is the interesting tension / trade-off between moving and attacking, and the high mechanical satisfaction gained from stutter-stepping / orbwalking (to borrow MOBA mechanics terms) that effectively weaves together dodging threats / repositioning and dishing out damage.

This is literally a game that can be played with one thumb, but it can feel very satisfying with a good amount of depth and skill expression. At any moment in time, players are reading the dynamic battlefield for upcoming threats, and making rapid decisions around optimal positioning.

The roguelike elements play nicely into content replayability. Players are offered random power-up choices (from a pool of skills) as they level up in a single run. These choices loosely constitute a “build”, though that is an under-utilized design space in this game in my opinion – there are skills that are clearly more powerful and are almost always prioritized. Despite this, the sheer RNG nature does provide lots of variability to each run, with the usual satisfaction highs/lows of RNG.

(A side note, the core gameplay largely holds up, but sometimes can get into a degenerate, unreadable state visually due to too many projectiles on-screen.)

Meta loop

The meta-game loop is where this game could really be upgraded. Core game content is segmented into “Chapters” of increasing difficulty (enemies with tougher mechanics and higher stats). Your character has permanent progression through gear (which can be dropped through play or loot boxes, can be fused to a higher rarity, and leveled up) and persistent stats power-ups.

The stats power progression (and thus, monetization of power) is really steep. A casual glance at Reddit shows most players talking about being stuck on Chapter 7 for weeks on end. (I’m stuck on Chapter 5 after a week’s play, with no monetization.) This is where the game sort of falls apart – the loop becomes a very long grind (farming earlier chapters) for gear drops, so that you can fuse / level-up to increase your stats, so that eventually you meet the power level to beat the chapter you are stuck at.

So why is it implemented like this, and how can it be better? If I were to speculate, this is likely a content production problem, with the small team making a conscious trade-off of using a steep power progression in place of a content treadmill they can’t keep up with. In other words – for live-ops there’s better churn/LTV by forcing players to farm for months vs. players cruising through the content and “completing the game”.

There are a bunch of systems that can be introduced to partially alleviate this. A random daily quest system would go a long way to introduce variety and make farming more tolerable. Social features are an entirely untapped space as well. For a small team though, these are likely substantial engineering challenges, so I don’t begrudge the team for not taking them on already.

Watch this space

My overall feeling from a couple of weeks’ play is this is likely a core gameplay concept that will be lifted by another studio with a larger budget, and married with a more mature meta loop. This is very much a diamond in the rough.